Suez Canal Crisis: Here Are The Cargoes In The Crossfire

By Greg Miller

FreightWaves

The “slow boat from China” just got a lot slower. Shipping sentiment toward the Suez Canal grounding of the Ever Given has taken a major turn. Operators are now opting to bypass the traffic jam and take the long detour around Africa’s Cape of Good Hope.

Ship-positioning data already confirms abrupt turns toward the cape by multiple ships. Container ships such as the HMM Rotterdam, Ever Greet, Maersk Skarstind and Hyundai Prestige; the crude tanker Marlin Santorini; and the liquefied natural gas (LNG) carrier Pan Americas, among others, have made beelines toward the cape. If the Ever Given is not refloated at high tide on Sunday, many more detours are expected.

There were 237 ships stuck at anchor awaiting canal transits as of Friday, according to Egypt’s Leth Agencies. That’s up sharply from 156 the day before.

Global ocean trade is fluid. The Suez Canal closure doesn’t block cargo. It changes the arrival date. The extent of delays from rerouting depends upon port pairs and vessel speed. A container ship traveling at 17 knots passing India en route from China to Rotterdam would take nine more days on the cape route than using the canal. If its destination was Italy, it would take 13 more days.

The double whammy of the canal queue and rerouting delays renders the global shipping network less efficient. The same ship capacity will not move the same cargo volume in the same time frame.

This will have a wide range of effects — some bad, some good — for shippers, vessel operators and investors.

Different segments, different exposures

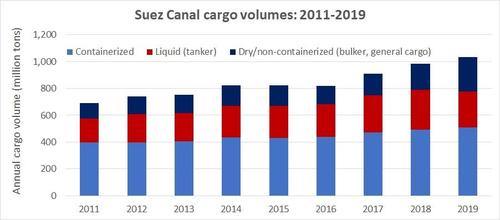

To gauge potential consequences, American Shipper analyzed historical data from the Suez Canal Authority (SCA) and obtained more recent data from trade-intelligence companies VesselsValue and Kpler.

The SCA data is a year old but shows the long-term trends. American Shipper separated SCA’s cargo data into three categories: containerized volume, dry cargo volume (bulkers and general cargo) and liquid (tanker) volume.

Total cargo volume grew 49% from 2011 through 2019. Containerized cargo is by far the most important. It comprises half the total, with liquid and dry bulk splitting the rest. But dry bulk volumes have grown the fastest. From 2015 through 2019, tanker volumes rose 13%, containerized cargo 18% and dry cargo 64%.

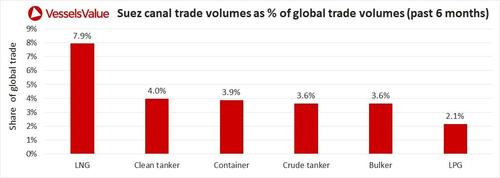

Another way to look at Suez Canal volume is in relation to global trade volume. VesselsValue provided American Shipper with this analysis, covering volumes over the past six months.

According to Adrian Economakis, chief strategy officer of VesselsValue, “Based on observation of our real-time and historical laden vessel activity, cargo volumes going through the Suez Canal accounted for around 4% of global trade over the last six months.

“The big question for the companies that control vessels on their way to Suez is to risk it and keep going or take the long way round. Either one will add delays and costs,” said Economakis.

Container capacity gets even tighter

The container sector faces the most systemic fallout from the Suez Canal accident.

Consider the case of the massive container-ship traffic jam in San Pedro Bay off Los Angeles and Long Beach. Since the beginning of the year, around 30 container ships have been stuck at anchor per day. They face delays of one to two weeks before reaching terminals. As of Thursday, there were still 29 ships at anchor in San Pedro Bay.

Now consider that the Ever Given accident has suddenly created an even bigger version of the California container-ship traffic jam. Leth Agencies reported that 53 container ships were at anchor awaiting passage through the Suez Canal on Friday. And that’s only half of the equation. All of the container ships taking the longer route around the cape are adding one to two weeks to their journeys.

While most of the container services via the Suez are Asia-North Europe and Asia-Med trades, everything is connected. The trans-Pacific trade relies on availability of container equipment. The Suez crisis will keep much-needed box equipment out of circulation for an extended period.

This will make equipment in Asia scarcer for U.S. importers at the very time demand is expected to intensify due to federal stimulus checks. Whether coincidence or not, Asia-West Coast rates (SONAR: FBXD.CNAW) just hit a new all-time high of $5,151 per forty-foot equivalent unit (FEU) on Thursday, according to the Freightos Baltic Daily Index.

Container stock outlook

The Suez crisis will add significant costs for liner companies serving the Asia-Europe trade. Rerouting around the Cape of Good Hope saves on canal tolls but heavily inflates fuel bills. The Suez snarl will also put upward pressure on ship and equipment leasing rates.

Stifel analyst Ben Nolan maintained that the Ever Given accident is “bad news” for liners. Diversions are “likely to be much more expensive and tie up equipment that could otherwise be making record profits.”

How much of the added costs can liners pass along to cargo shippers? Carriers could institute a surcharge for cargo diverted around the cape. Spot rates could remain elevated for longer — or even increase. In addition, the Suez Canal incident could give liners even more sentiment ammunition in their annual contract negotiations with shippers.

The Ever Given accident is overwhelmingly good news for shipowners that charter vessels to liners: companies such as Danaos, Costamare, Global Ship Lease, Navios Partners and Capital Product Partners.

“Shipowners … who were already in a terrific competitive position are in an even stronger competitive position, at least for the time being,” explained Nolan.

The same goes for box-equipment lessors Textainer, CAI International and Triton International.

B. Riley Securities analyst Daniel Day hiked his box-lessor price targets after the Ever Given grounding. “We now expect container shortages to last through at least Q2 and [to be] increasingly likely for the majority of 2021. A worst-case scenario [in the Suez Canal] could result in new record highs for new container prices,” he said.

Less upside for crude tankers

The Suez Canal is not as important as it used to be for tanker shipping. Nevertheless, a blockage that lasts weeks not days would certainly be a plus for rates, particularly for product tankers.

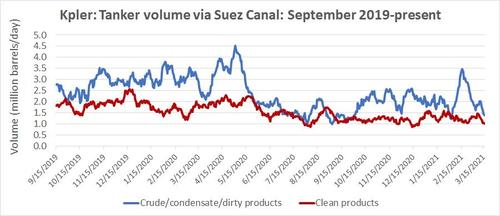

Data on tanker flows through the canal was provided to American Shipper by Kpler.

The data shows a fall in volumes for both crude and clean products as COVID reduced demand and OPEC+ cut production. Crude volumes spiked in April 2020 when the OPEC+ agreement briefly broke down. There was a bump last month due to Iraqi crude moving west combined with Russian crude headed east.

The effect of the Ever Given accident on crude-tanker demand is limited for two reasons. First, a large portion of the global trade already sails around the Cape of Good Hope using very large crude carriers (VLCCs; tankers that carry 1 million barrels). Second, the SUMED pipeline from the Red Sea to the Mediterranean allows northbound crude flows to circumvent the canal.

Nolan added, “Crude-tanker markets are currently so oversupplied and depressed that even a 3-5% increase in utilization [due to ship diversions], while helpful, is unlikely to tip the balance of supply and demand.”

More upside for product tankers

The main product-tanker flows through the canal are naphtha headed east to Asia and diesel and other refined products headed west to Europe.

Potential product-tanker upside from the accident would have been greater if not for a new wave of COVID lockdowns in Europe, reducing transportation-fuel demand. Even so, analysts are more optimistic on this segment than on crude tankers.

According to Nolan, “We expect the impact could be more meaningful for product-tanker markets, specifically the larger LR2s [product tankers with capacity of 80,000-119,000 deadweight tons or DWT] that move a great deal of the product exported from Middle Eastern refineries. Not all of this goes through the Suez Canal. But the product-tanker market was not as oversupplied as the crude-tanker market. So, we do expect that a change in freight efficiency could have a more dramatic impact on product-tanker freight rates.”

Nolan noted that of the public companies, Scorpio Tankers (NYSE: STNG) has the most LR2 exposure.

Clarksons Platou Securities reported on Friday that rates for 2010- to 2014-built LR2s jumped 21% compared to Thursday, to $20,700 per day. Rates for LR2s built in 2015 or later surged 18% day-on-day, to $24,000 per day.

According to Clarksons analyst Frode Mørkedal, “Brokers report that the list of available LR2s in the West [Western Hemisphere] is very tight and that charterers’ options are severely limited, thus pushing freight rates upwards. This is a trend that is expected to continue due to the lack of ship supply coming from the East, especially with the current Suez situation leading to further delays.”

As Alphatanker put it, “The longer the disruption lasts … the tighter the tonnage lists will become, especially for large clean tankers.”

Rate tailwinds for dry bulk

Container shipping and tankers are garnering the headlines. But as the SCA statistics revealed, there’s a dry bulk angle as well.

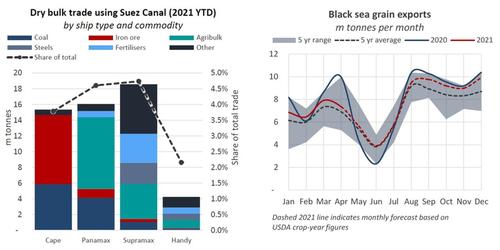

The first quarter has already been incredibly strong for bulkers in the Panamax (65,000-90,000 DWT) and Supramax (45,000-60,000 DWT) segments. Rates for these bulkers are at decade-highs.

Nick Ristic, lead dry cargo analyst for Braemar ACM Shipbroking, sees potential upside for both Panamaxes and Supramaxes as a result of the canal accident. Both markets are already tight.

Two-thirds of all Panamax ships sailing from the Black Sea traversed the Suez Canal in 2020 “and for grains specifically, this figure was 73%,” he wrote in his latest market outlook. Braemar expects an additional 7.4 million tons of Black Sea grain to be shipped in the current season. “With Chinese demand for grains still extremely high, prolonged Suez closures could translate to more of these ships taking the long route to the Far East,” he said.

Meanwhile, Supramaxes are heavily exposed to the steel trade from Asia to the Atlantic Basin. Steel exports in Q1 2020 are at half-decade highs, driven by China and South Korea. Import demand “is extremely high,” noted Ristic, who said that “bumper trade flows” and diversions due to the Suez closure could “tighten the market further.”

MORE ON SUEZ CANAL CLOSURE: What the Suez canal accident means to the tanker business: see story here. Everyone wants to talk — or laugh about — the Suez Canal crisis: see story here. Scores of container ships waiting to transit Suez Canal: see story here.

___

https://www.freightwaves.com/news/suez-canal-crisis-here-are-the-cargoes-in-the-crossfire