SOTN Editor’s Note: While the following exposé is as detailed and accurate as they come, it’s important to understand that there are multiple levels of unseen otherworldly power situated above those delineated below. Those extremely powerful entities, which exert complete command and control over the Illuminati family bloodlines, Northern Italian Black Nobility, Khazarian Cabal, Talmudic Freemasonry, Neocon Zionists, Committee of 300, etc., operate from off-planet extraterrestrial civilizations and have been given their positions of domination over the human race … but only temporarily. Variously known as the Archons, Annunaki, Dracos, Greys, Reptilians, Fallen Angels, etc., these different groups of quite real aliens have basically been put in charge of running Earth as a prison planet. Which meant that the entire planetary civilization had to be meticulously set up as a financial and economic penitentiary as it is today.

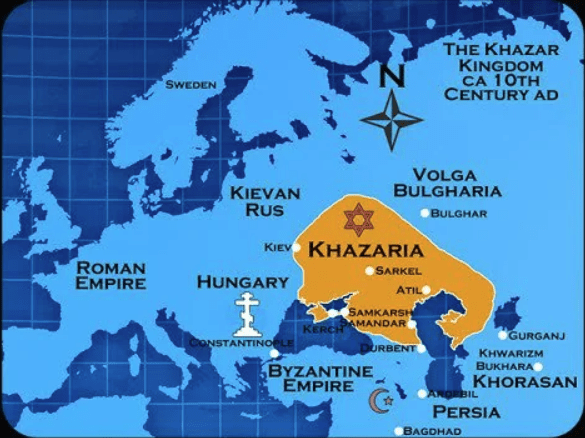

It’s crucial to comprehend the true breadth and depth of this once highly secret global power structure. And it’s even more critical to properly understand the genesis of the most recent version and international criminal conspiracy to rule the realm. One could say that the satanic lockdown which began in the modern era had its roots in the Khazar Khaganate, which was located from Kiev, Ukraine to Atil or Itil, the Khazar capital on the Volga (see map above). However, this reality in no way diminishes the over-riding significance of the Babylonian Radhanites who preceded by thousands of years the Khazarians. Nevertheless, it’s absolutely essential, especially in light of the potentially apocalyptic Ukraine War, to correctly apprehend both the position and the role of the Khazarian Cabal within today’s world power pyramid. That begins with knowing their once extremely secret back story which has been effectively covered up for centuries until 2015. As follows:

How the Khazarian Cabal has controlled Ashkenazi Jewry

so it can rule planet Earth from behind the veil

Folks, please do not gloss over the vital “Khazarian” content found in the preceding link. For it well explains what is found no where else on the Internet today. It even discloses the actual reason for the extraordinary construction of the Great Pyramid of Giza, an ‘impossibility’ even applying today’s most advanced technologies and sophisticated equipment.

As a highly regarded revisionist historian once noted:

“If you understand the real purpose of the Great Pyramid of Giza, then you will understand all of human history going back to Atlantis.”

State of the Nation

March 21, 2023

N.B. What follows is the excellent disquisition of the historical record which clearly identifies the key players in this multi-millennia, mega-crime MAMMON drama. These are the bad actors were used throughout history to create the current global state of affairs defined by so much pervasive crime and profound corruption.

THE HISTORY OF MONEY, WARLORD BANKSTERS, AND THE WORSHIP OF MAMMON

THIS REPORT IS ALSO AVAILABLE AS A PDF: History-of-Warlord-BankingDownload

By Douglas Gabriel

Aim4Truth.org

The path of the Warlord Banksters is complex and has been hidden by obfuscation, deceit, and subterfuge to obscure the truth and protect a small group of banking families whose scams have fleeced every nation on earth and hidden the loot in offshore tax havens that hold the stolen wealth of the world. These elite banking families own the controlling interests in the Fortune 500 companies through asset management companies, shell corporations, offshore accounts, and a thousand other “old banking tricks” that have been used since the time of King Hammurabi of Babylon. The Italian, Jewish, German, and Lombard bankers of Venice used the same old tricks of the “father of lies” to create privately owned central banking systems that are used to this day in most countries and still owned by the same self-aggrandizing banking families.

Greed, known as the evil demon “Mammon”, hasn’t changed his ways since the cut-throat machinations of the Medici bankers laid down the principals of corporate warlord banking that are inherently immoral and work against human advancement by engendering war, predatory banking, and economic slavery.

Ultimately, these “usury bankers” convinced governments to lock people up for not paying back loans on time. “Debtor’s Prison” was the outcropping of banking families, later called merchant bankers, controlling governments and economies that reached beyond “national” limitations. As commerce, trade, and mercantilism took over the world, bankers continued to have the upper hand and indeed made and destroyed kings and kingdoms with loans from their family banks. These families became corporate lineages that are still in power throughout the world today and associate through the Pilgrims Society, World Economic Forum, IMF, World Bank, BIS, and many secret cabals, like: the Vatican and British Knights of Malta, CFR, RIIA, the United Nations, and many other elite globalist groups.

THE INVENTORS OF BANK FRAUD AND THE DEMISE OF BABYLON

Money was first developed in the ancient world in temples that kept track of the storage of grain and food for the next season, which was initially a good and moral intention that charged no service fee or interest. Coins and money were developed to represent the value of human labor and stored resources. Eventually, temples began to use their excess grain stores, and hard coins, to make loans to others as investments. This money was used for the benefit of the group, not the personal gain of the individual. When the control of money left the domain of the temple, the positive uses for surplus grain and coin were “turned to the dark-side”, and demons began fighting with the gods of the temple for the control of money and the lives of the people. Until we have the full picture of the evolution of money (Mammon), we will be unconsciously subject to these powerful demonic forces that are controlling our personal and global economic lives.

The story of money in the Western world begins around 2000 BC when the Babylonians had evolved into a highly developed commercialized society, complete with a sophisticated monetary and credit system. Barley and silver functioned side by side in a dual monetary system that made use of both as mediums of exchange and standards of value. Historically, barley preceded silver as the chief form of currency. A legal ratio established the value of silver in terms of barley and vice versa. Creditors accepted payments in either silver or barley, depending upon a debtor’s preference. Silver grew in importance relative to barley, and later Babylonian gold became a competing metal currency.

The Code of Hammurabi (2123-2108 BC) specified grain money for certain payments and metal for others. Merchants who insisted upon payment in the wrong currency could face severe penalties. The standard monetary unit was a shekel, equal to 180 grains of barley, or a fixed weight of silver. Silver was melted into small ingots that circulated as money and was usually tested for fineness at each transaction. Some of the ingots bore the image or super-scription of the god whose temple guaranteed the fineness of the silver.

Temples lent goods from their stores for repayment in-kind as a general practice. These loans charged no interest as long as they were repaid on time. Some merchants carried on a banking business of sorts, making loans in silver and grain, and holding deposits of customers that earned interest. These customers could pay obligations by writing drafts on these deposits. The statutory rate of interest was 20 percent, but silver loans often earned 25 percent and grain loans more than 33 percent. Bills of exchange were carved on clay tablets.

It is believed that traders began marking their own shekels in order to avoid the time-consuming process of weighing each transaction. Merchants who “issued” their own shekels could then trade them to patrons as IOUs. Any returning customers could then trade the marked shekel for a quantity of goods or services and the merchant would know that their standard weight secured the payment. This method eventually developed into a coinage system where rulers and states developed their own sovereign currency as a standard for exchange.

BABYLONIAN BANKING

Since land was such an essential part of Babylonian life, banking firms at the time were heavily involved in real estate matters. Banking firms like the House of Egibi acted as land managers, renting fields for absentee landlords, while other firms dealt strictly with royal-owned lands. For example, the House of Murashu, operating in the last half of the 5th Century BC, became successful by “renting royal lands to tenant farmers and acting as agents in converting agriculture profits into metal.”

With prosperity came merchant bankers and a larger sector of the population participating in commercial and financial operations, whose transactions were based on a silver standard and modeled on promissory notes.

Contracts were written including a notarization by witnesses with the location and date. Goods would be weighed in silver and totaled for an amount payable which could be loaned to the purchaser. After a debt was repaid, the creditor would break the promissory clay tablet.

Private Babylonian banks also supported venture capitalists seeking commercial enterprises. A group of investors would pool their resources and give the capital to an individual to carry out commercial transactions to make a profit that would be divided among the initial investors, thus the model for corporations came into being.

In Babylon, at the time of Hammurabi, there are records of loans made by the priests of the temple. Temples took in donations and tax revenue and amassed great wealth. They redistributed these goods to people in need such as widows, orphans, and the poor and allowed people to take interest-bearing loans. The loans were made at reduced below-market interest rates. Sometimes arrangements were made to make food donations to the temple instead of repaying interest.

Once these systems of usury were established and the grip of Mammon was creating a cultural transformation based upon money, people naturally fell into debt and became slaves to pay off their debt.

The debtor being imprisoned for debt could nominate his wife, a child, or slave to work off the debt. The situation got so out of hand that King Hammurabi decreed that no one could be enslaved for more than three years for debt. Other cities, with residents racked by debt, issued moratoriums on all outstanding bills. The worship of Mammon was taking hold of the cultures that embraced usury and focused on “money that makes money from no labor” – evil usury.

During the 5th century BC, “Warlord Banking Families” came into existence in Babylon in their initial form; the Houses of Egibi, Murashu, Ea-iluta-bani, and Borsippa were such banking families. These “banksters” were classified as “merchant bankers” but should be seen as worshipers of Mammon who turned culture significantly toward materialism and belief in greed and harmed and killed many people in the process.

MAMMON – THE DEVIL BEHIND MONEY

Mammon in the New Testament of the Bible is commonly thought to mean money, material wealth, or any entity or devil that promises wealth and is associated with the greedy pursuit of personal gain and self-aggrandizement. In the Middle Ages, Mammon was often personified as a demon and sometimes included in the seven princes of Hell who govern the “Seven Deadly Sins.” Mammon in Hebrew means “money” and is the god of material things, essentially the “materialism” of our time that seems to control most Westerners.

The Seven Deadly Sins lead to Hell, and Mammon is seen as one of the most powerful demons who herds humanity on the paths of perdition.

The Seven Deadly Sins and their accompanying demons are often listed as:

Lucifer: Pride

Mammon: Greed

Asmodeus: Lust

Leviathan: Envy

Beelzebub: Gluttony

Satan: Wrath

Belphegor: Sloth

The word mammon can denote wealth or profit in the original Syriac dialect but also is the name of a Syrian deity who was the god of riches. The Mishnaic Hebrew word mamôn means money, wealth, possessions, and “that in which one trusts.”

Eventually, due to the Christian injunction against charging interest for money that is loaned to another person (usury), the entire idea of money (mammon) became a pejorative, a term that was used to describe pride, greed, gluttony, excessive materialism, and unjust worldly gain. The “worship” of money was seen as a sin, and the work of the demon of greed, Mammon. Later, money becomes synonymous with hellish intent and bondage to the physical world which leads humans into the dark realms; therefore, Christians were warned to stay away from practices of usury and the glorification of Mammon. It was a common belief that usury is the work of the devil and certainly not fit for a Christian. A Christian should be faithful with “another” and help them out of love, not for the purposes of money mongering for personal gain. The Christian is careful not to be contaminated by the “unrighteousness” of wealth and money and the lure of Mammon.

The appearance of the demon of money and greed has changed over time. Mammon is now a card credit or a PIN for your bank account, check, cash, Bitcoin, direct deposit, or a debit or credit to your account digitally. The materialism that created Mammon is so engrained in Westerners that it is subconscious background noise that is seldom noticed. Mammon rules the human will-power through tax-debt slavery, technological assaults on human lifestyles, and control of human addictions. The Seven Deadly Sins are found in most Hollywood productions and the path to Hell is like a red carpet rolled out for “warlord bankers and brokers” who lavish themselves in the pride of greed, gluttony, lust, hatred, and war. Mammon is global big-business, and the banking families aren’t giving up any money without good returns on their investments, onerous usury, and global control of the flow of money.

It is probably fair to say that most Westerners are either overwhelmed with this system of Mammon or are blissfully ignorant and wallowing in the pigsty of materialism. It is a comfortable mud-hole with scraps from the bankster elites to please the middle-class palette. Since Westerners have little understanding of the true history of the world, there is little or no understanding of the economic system of control that got us to this current insane, economically controlled world where America owes banking families $25 trillion in debt through the U. S. Federal Reserve which creates continuous onerous debt that can never be paid off. Ever rising debt is the usual method that banksters (economic gangsters) use to control entire countries through war debt — wars that the warmongering banksters often help to create.

WARLORD BANKERS

The first “modern” bank was established in Venice with a guarantee from the State in 1157 AD and operated until 1797 acting in the interest of the Crusaders of Pope Urban the Second. This activity developed into the Bank of Venice, with an initial capital of 5,000,000 ducats. This bank was the first national bank to have been established within the boundaries of Europe.

In the middle of the 13th Century, when certain rich Italian families saw the profits that the Venetian banking families were making, groups of Italian Christians, particularly the Cahorsins and Lombards, invented “legal fictions” to get around the ban on Christian usury. One method of Christians effecting a loan with interest without calling it usury was to offer money without interest, but also require that the loan is insured against possible loss or injury, and/or delays in repayment. The Christians effecting these legal fictions became known as the Pope’s Usurers and reduced the importance of the Venetian and Italian Jews to European monarchs.

The most powerful Italian warlord banking families came from Florence, including the Acciaiuoli, Mozzi, Bardi, and Peruzzi families, which established branches throughout Europe. Probably the most famous Italian bank was the Medici bank, set up by Giovanni di Bicci de’ Medici in 1397 and continuing until 1494.

The spread of Italian bankers into Europe was dramatic. By 1327, Avignon, France, had 43 branches of Italian banking houses. The accompanying growth of Italian banking in France was the start of the Lombard moneychangers in Europe, who moved from city to city along the busy pilgrim routes important for trade. By the later Middle Ages, Christian merchants who lent money with interest were without opposition, and the Jews lost their privileged position as moneylenders.

After 1400, political forces turned against the methods of the Italian free enterprise bankers and in 1401, King Martin I of Aragon had some of these bankers expelled. In 1403, Henry IV of England prohibited them from taking profits in any way in his kingdom. In 1409, Flanders imprisoned and then expelled Genoese bankers. In 1410, all Italian merchants were expelled from Paris.

Later, when modern banking practices became widespread, the Italian banking families became prominent again, especially between 1527 and 1572 when Italy produced a number of important banking family groups: the Grimaldi, Spinola, Pallavicino, Doria, Pinelli and Lomellini.

The Bardi, Peruzzi, and Acciaiuouli family banks, along with other large banks in Florence and Siena in particular, were all founded in the years around 1250. In the 1290s they grew dramatically in size and rapaciousness, and were reorganized, by the influx of new partners. These were “Black Guelph” noble families, of the factions of northern Italian landed aristocracy, were always bitterly hostile to the government of the Holy Roman Empire. Charlemagne, 500 years earlier, had already recognized Venice as a threat equal to the Vikings, and had organized a boycott to try to bring Venice to terms with his Empire. Venice in 1300 was the center of the Black Guelph faction which drove Dante and his co-thinkers from Florence. Machiavelli describes how by 1308, the Black Guelph ruled everywhere in northern Italy except in Milan, which remained allied with the Holy Roman Empire, and was the most economically developed and powerful city-state in fourteenth century Italy.

The charter of the Parte Guelfa openly claimed that it was the party of the papacy, and with Venice, the Black Guelph openly pushed for the Popes to change usury from a mortal sin to a venial sin. The Venetians seemed to enjoy an effective exemption from the Catholic Popes injunctions against usury, and also from their ban on trading with the infidel — the Seljuk and Mamluk regimes of Egypt and Syria.

A century earlier, in the 1180s, Doge (Duke) Ziani of Venice had Emperor Frederick agree to withdraw his standard silver coinage from Italy and allow the Italian cities to mint their own coins. Over the century from the 1183 Peace of Constance to the 1290s, Venice established the extraordinary, near-total dominance of trading in gold and silver coin and bullion throughout Europe and Asia.

The Black Guelph bankers of Florence did not simply loan money to monarchs and then expect repayment with interest, because interest was often “officially” not charged on the loans, since usury was considered a sin and a crime among Christians. The primary conditionality was the pledging of royal revenues directly to the bankers — the clearest sign that the monarchs lacked national sovereignty against the Black Guelph “privateers.” Since in fourteenth century Europe important commodities like food, wool, clothing, salt, iron, etc. were produced only under royal license and taxation, bank control of royal revenue led to, first, private monopolization of production of these commodities, and second, the banks’ “privatization” and control of the functions of royal government itself.

By 1325, the Peruzzi bank owned all of the revenues of the Kingdom of Naples (the entire southern half of Italy, the most productive grain belt of the entire Mediterranean area); they recruited and ran King Robert of Naples’ army, collected his duties and taxes, appointed the officials of his government, and above everything sold all the grain from his kingdom. They egged Robert on to continual wars to conquer Sicily, because through Spain, Sicily was allied with the Holy Roman Empire. Thus, Sicily’s grain production, which the Peruzzi did not control, was reduced by war.

King Robert’s Anjou relatives, the Kings of Hungary, had their realm similarly “privatized” by the Florentine banks in the same period. In France, the Peruzzi were the cooperating bank of the bankers to King Philip IV. The Bardi and Peruzzi banks, “privatized” the revenues of Edward II and Edward III of England, paid the King’s budget, and monopolized the sales of English wool.

When King Edward tried forbidding Italian merchants and bankers from expatriating their profits from England, they converted their profits into wool and stored huge amounts of wool at the monasteries of the Order of Knights Hospitalers, who were their debtors, political allies, and partners in the monopolization of the wool trade. It was the Bardi’s representatives who proposed to Edward III the wool boycott which destroyed the textile industry of Flanders.

Large revenue flows came to the Vatican in the collection of its church contributions and tithes. Under John XXII, the Black Guelph Pope from 1316-1336, papal tithes sky-rocketed reaching the apparent value of 250,000 gold florins per year. All were collected by agents of the Venetian banks (for France, the largest source of papal revenue) and the Bardi Bank (for everywhere else in Europe except Germany). They charged the Vatican sizable “exchange fees” to transfer the collections.

Only the Venice-allied bankers had the reserves of cash to finance papal operations. They transferred collections from Europe and loaned them to the Popes in advance. Thus, Venice controlled the papal credit and the continuing hostilities between the papacy and the Holy Roman Emperors.

In the Italian city-states themselves, the early years of the fourteenth century saw the assignment of more and more of the revenues of the primary taxes to the bankers and other Guelph Party bondholders. From about 1315, the Guelph abolished the income taxes in the city, but increased them on the surrounding rural areas into which they expanded their authority. The bankers, merchants, and wealthy Guelph aristocrats did not pay taxes, but instead, they made loans to the city and governments.

Some of the famous banks of Tuscany had failed already in the 1320s: the Asti of Siena, the Franzezi, the Scali company of Florence. In the 1330s, the biggest banks, with the exception of the Bardi, the Peruzzi, Acciaiuoli and Buonacorsi, were losing money and plunging toward bankruptcy with the fall in production of the vital commodities which they had monopolized. The Acciaiuoli and the Buonacorsi, who had been bankers of the Vatican before it left Rome, went bankrupt in 1342 with the default of the city of Florence and the first defaults of Edward III. The Peruzzi and Bardi, the world’s two largest banks, went under in 1345, leaving the entire financial market of Europe and the Mediterranean shattered with the exception of the much smaller Hanseatic League bankers of Germany, who had never allowed the Italian banks and merchant companies to enter their cities.

VENICE, THE WORLD’S MINT

Between 1250 and 1350, Venetian financiers built up a worldwide financial speculation in currencies and gold and silver bullion. This ultimately dwarfed and controlled the speculation in debt, commodities, and trade of the Bardi, Peruzzi, and the other banking families took all control of coinage and currency from the monarchs of the time.

The Venetian financial oligarchy as a whole, which ruled a maritime empire through small executive committees under the guise of a republic, centralized and supported its own speculative activities as a whole. The “Republic” built the ships and auctioned them to the merchants; escorted them with large, well-armed naval convoys of their empire, with naval commanders responsible to the Venetian “Committee of Ten” and the magistrates for the convoys’ safety. This same oligarchy maintained several public mints and did everything possible to foster the centralization of gold and silver trading and coinage in Venice which was the dominant trade of Venice by 1310. The Venetian banks and bullion-dealers were backed by large pools of capital and protection and worked out of the Cathedral of San Marcos’ Grain Office and the Procurators of San Marcos who controlled the collection of the taxes of the Republic.

The size of the Venetian bullion trade was huge: twice a year a “bullion fleet” of up to 20-30 ships under heavy naval convoy, sailed from Venice to the eastern Mediterranean coast or to Egypt, bearing primarily silver; and sailed back to Venice bearing mainly gold, including all kinds of coinage, bars, leaf, etc. The profits of this trade put usury to shame.

The Christian Crusades (the first in 1099, the seventh and last major one in 1291) had only one strategic effect: expanding and strengthening the maritime commercial empire of Venice to the East. Venice provided the ships to take the crusaders to the Middle East; Venice loaned them money, and Venetian Doges often told them what cities to try to capture or sack. Through the crusades, Venice gained effective control of the cities of Tyre, Sidon, and Acre in Lebanon and Lajazzo in Turkey, and strengthened its domination of commerce through Constantinople. These were the coastal entry-points through the Black Sea and Caspian Sea regions to China and India.

The strategic alliance between Venice and the Mongol Khans gave Venice huge amounts of gold with which to dominate world currency trading for decades. Mongol middlemen met Venetian merchants at the Mongol-ruled Persian trading cities of Tabriz, Trebizond, and Tana trading gold for silver from Europe. A large-scale trade in slaves from Mongol domains was associated with this currency trading. The Venetians were able to raise the price of silver despite the existence of record quantities coming to Venice from Europe. The crusades also consolidated the alliance of Venice and its allied Black Guelph-ruled cities, the Papacy, and the Norman and Anjou kings against the Holy Roman Empire centered in Germany.

In the late thirteenth and fourteenth centuries, Venice provided all the coinage and currency exchange for the largest empire in history, which was looting and destroying the populations under its rule. Venice had taken over the currency trading and coining of what remained of the Byzantine Empire. Venice, over this period, took the East off a gold standard and put it on a silver standard. It took Byzantium and Europe off a 500-year-old silver standard and put them on gold standards.

The Venetian financiers and merchants were making annual rates of profit of up to 40 percent on very large, overwhelmingly short-term (six-month) investments. Venice ensnared all the surrounding economies, including the German economy where production of silver, iron, and iron implements was concentrated. By the 1320s, Venetian merchants no longer travelled to Germany to trade. They compelled German producers and merchants to come to Venice and take up lodgings in the “Warehouse of the Germans” where their goods were stored for sale. Venetian bankers on the Rialto (del Banco) made cashless bank transfers among merchants’ accounts, allowed overdrafts, gave credit lines on the spot, created “bank money,” and then speculated with it. They did this out of thin air by simply controlling currency speculation worldwide because they controlled the currency and had the reserves to back it up.

The Rialto bankers charged fees to those involved in trade because exchanging currencies might be involved in a transaction. These exchange fees were taken out of production and trade costs that hurt profits while the usury profits made the bankers ever richer. Then, the bankers made the “bills of exchange” even more expensive, to hedge against their own potential losses in currency fluctuations being manipulated by Venetian bullion merchants. Thus, bills of exchange in the fourteenth century cost 14 percent on average, worse than borrowing money at the set interest rate. Ultimately, the Rialto del Bancos always gained more wealth from every deal, until of course, they went bankrupt.

Venice switched Europe to gold by looting silver. England, for example, from 1300-1309 imported 90,000 pounds sterling in silver for coining; but from 1330-1339, it was only able to import 1,000 pounds. But in Venice there was no lack of silver at all in the 1330s. The Florentine bankers, with their famous gold florin, enjoyed great speculative profits in this currency scam.

After 1400, political forces turned against the methods of the Italian “free enterprise” merchant bankers. In 1401, King Martin I of Aragon (Spain) expelled them. In 1403, Henry IV of England prohibited them from taking profits in any way in his kingdom. In 1409, Flanders imprisoned and then expelled Genoese bankers. In 1410, all Italian merchants were expelled from Paris. When Louis XI became King of France in 1461, he organized national forces to make it the first strong and sovereign nation state. Along with the development of ports, roads, and support for the cities, Louis XI insisted on a single, standard national currency, created and controlled by the crown. For both Louis XI and England’s Henry VII in the same period, mercantilist forms of economic nationalism were combined with a pronounced hostility to Italian techniques of credit and clearing.

ITALIAN BANKSTERS FLEE TO GERMANY

In Germany, we find many Italian banking families migrating to Hamburg and becoming the hidden money behind the Hanseatic League, an early trading company that used Spanish and Portuguese merchant sailors in the lucrative spice and slave trade. These early unions of rich bankers investing in trade became the basis for what would become corporations like the Dutch and British East India companies and the model for European central banks. In southern Germany, two great banking families emerged in the 15th Century, the Fuggers and the Welsers. They basically came to control much of the European economy and dominated international high finance in the 16th Century. The Fugger Bank lasted from 1486 to 1647 and Jacob “the rich” Fugger (originally spelled “Fucker”) became the richest man in history.

Also important to the Northern German city states establishing powerful banks was the influence of Dutch bankers. Berenberg Bank is the oldest bank in Germany and the world’s second oldest bank, established in 1590 by Dutch brothers Hans and Paul Berenberg in Hamburg. The bank is still owned by the Berenberg banking family.

Throughout the 17th Century, precious metals from the New World, Japan, and other locales were being channeled into the Bank of Amsterdam. The Netherlands attracted coin and bullion to be deposited in their banks until they became a leading force of banking. The concepts of fractional-reserve banking and payment systems were developed and spread to Germany, England, and elsewhere from Holland.

In the City of London, the London Royal Exchange was established in 1565. By the end of the 16th Century and during the 17th, the traditional banking functions of accepting deposits, moneylending, money-changing, and transferring funds were combined with the issuance of bank debt that served as a substitute for gold and silver coins. This would lead to government regulations and the first central banks in Europe. The success of the new banking techniques and practices in Amsterdam and London helped spread the concepts and ideas elsewhere in Europe. The convenience of modern banking was becoming such a way of life that the modern person couldn’t really exist without a bank account. Thus, the grip of Mammon became stronger and yet more unconscious as banking practices entered daily life more and more.

MODERN BANKING

The original modern banks were “merchant banks” that Italian grain merchants invented in the Middle Ages. As Lombard merchants and bankers grew in stature, based on the strength of the Lombard plains cereal crops, many displaced Jews fleeing Spanish persecution were attracted to the trade of banking in Italy.

Jews could not hold land in Italy, so they entered the great trading piazzas and halls of Lombardy, alongside local traders, and set up their benches (bancos) to trade in crops. They had one great advantage over the locals. Christians were strictly forbidden the sin of usury, defined as lending at interest. The Jewish newcomers, on the other hand, could lend to farmers against crops in the field, a high-risk loan at what would have been considered usurious rates by the Church; but the Jews were not subject to the Church’s dictates. In this way, they could secure the grain-sale rights against the eventual harvest. They then began to advance payment against the future delivery of grain shipped to distant ports. In both cases they made their profit from the present discount against the future price. This two-handed trade was time-consuming and soon there arose a class of merchants who were trading grain debt instead of grain.

The Jewish trader performed both financing (credit) and underwriting (insurance) functions. Financing took the form of a crop loan at the beginning of the growing season, which allowed a farmer to cultivate his annual crop. Underwriting in the form of a crop (commodity) insurance guaranteed the delivery of the crop to its buyer, typically a merchant wholesaler.

Merchant banking progressed from financing trade on one’s own behalf to settling trades for others and then to holding deposits for settlement of a “billette” or note written by the people who were still brokering the actual grain. And so, the merchant’s “benches” (banco-bank) in the great grain markets became centers for holding money against a bill. These deposited funds were intended to be held for the settlement of grain trades, but often were used for the bench’s (bank’s) own trades in the meantime through loans with high rates of interest. The broadening of merchant banker’s powers caused an imbalance in wealth that led the rich to lock-up the poor and bankers to turn the wheels of commerce into the gears of war.

In the 12th Century, the need to transfer large sums of money to finance the crusades stimulated the re-emergence of banking in western Europe. In 1162, Henry II of England levied a tax to support the crusades. The Templars and Hospitallers acted as Henry’s bankers in the Holy Land. The Templars’ large land holdings across Europe also emerged in the 1100–1300 timeframe as the beginning of Europe-wide banking, as their practice was to take in local currency, for which a demand note would be given that would be good at any of their castles across Europe and the Levant, allowing movement of money without the usual risk of robbery while traveling.

The Crusades became the platform for merchant banking families to become Warlord Banking Families, who are still fomenting war to this day so that they might benefit by loaning money to both sides of the war and make a handsome profit. Then, once the victor is known, the Warlord Bankers set up a central banking system to create currency that enslaves the victims of the war to a debt that can never be paid off. This central banking system assures that the “money” of a country or people becomes part of the larger system of Mammon worship that desires to have complete economic control of the world – hegemony, the ultimate outcome of greed.

A TIMELINE OF WARLORD BANKING FAMILIES

It is instructive to have a glossary of the Warlord Banking Families founders and early members to see that it truly is only a very few families that began the wholesale takeover of banking throughout the world. To understand history, we need a timeline of biographies, not just dates and times of historical events. Once we know the usual culprits, many pieces of the globalist’s puzzle fall into place.

Below are some of the European bankers who spread to America and infected the U. S. Federal Reserve with the same predatory banking practices that have been inspired by Mammon worship since ancient Babylon. You will recognize many of these bankers because their names come up as the money behind most “conspiracy theories.” Unfortunately, the City of London and its power is no conspiracy theory and the Warlord Bankers and Brokers who prey on nations for personal gain still have the upper hand and maintain economic slavery over most of the globe.

FAMOUS WARLORD BANKSTERS – MOST WANTED LIST

Acciaiuoli and Buonacorsi International Banks had been bankers of the Vatican before they left Rome and went bankrupt in 1342 with the default of the city of Florence and the first defaults of Edward III. The Peruzzi and Bardi, the world’s two largest banks, went under in 1345, leaving the entire financial market of Europe and the Mediterranean shattered, with the exception of the much smaller Hanseatic League bankers of Germany, who had never allowed the Italian banks and merchant companies to enter their cities.

Jakob Fugger (1459-1525) also known as Jakob Fugger the Rich or sometimes Jakob II, was a major merchant, mining entrepreneur, and banker of Europe. He was a descendant of the Fugger merchant family. He is considered to be the richest person in history.

Francesco Zorzi (Francesco Giorgi Veneto, 1466-1540) was an Italian Franciscan friar and author of the work De harmonia mundi totius (1525). The Cambridge History of Renaissance Philosophy describes him as ‘idiosyncratic’ and his works emboldened Italian banking families to dominate economic markets throughout Europe for centuries and justify their evil through the Church’s own philosophy. Zorzi’s influence cannot be overstated for he was quoted continuously by the Venetian school of central bankers who essentially came to control European economics.

Gasparo Contarini (1483-1542) was an Italian diplomat, cardinal, and Bishop of Belluno. He was born in Venice of the ancient noble House of Contarini. Contarini is one of the founding families of Venice and one of the oldest families of the Italian Nobility. In total, eight Doges to the Republic of Venice emerged from this family, as well as 44 Procurators (bankers) of San Marco, numerous ambassadors, diplomats, and other notables. Among the ruling families of the Republic, they held the most seats in the Great Council of Venice.

Anselmo Banco (Asher Levi Meshullam, d. 1532) was considered the Father of the Warburg family and was the acknowledged head of the Jewish community in Venice. Owner of several loan-banks in the Venetian territories, Anselmo took refuge in Venice (from which the Jews had been hitherto excluded) when Padua was sacked by troops of the League of the Cambrai in 1509. From then on, he acted as spokesman for Venetian Jewry and was largely responsible for securing rights of residence and taxation. He represented the community also in 1516 when the senate decided to establish a ghetto. He was also involved with the Jewish community of Jerusalem, sending money and helping those who sailed there from Venice. He corresponded with the famous kabbalist Abraham ha-Levi of Jerusalem on messianic subjects. The family members were proprietors of one of the seven Venetian synagogues, known as the Scuola Meshulamim. Some of their descendants settled in Warburg and Hamburg and were among the ancestors of the Warburg family.

Sir Horatio Pallavicini (1540-1600) was the son of an Italian merchant who was recommended to Queen Mary and appointed Collector of Papal Taxes. He abjured Romanism on Mary’s death and appropriated the sums collected for the Pope. He lent large sums of money to Queen Elizabeth as well as to the Netherlands and Henry of Navarre and was knighted by Queen Elizabeth I in 1579. His first son, Sir Henry, married Jane Cromwell while his other son Tobias married Catherine Cromwell. His daughter married Henry Cromwell, son of Oliver Cromwell. The power and influence of the Pallavicini banking family in England was extraordinary for hundreds of years and still has a tremendous influence as one of richest, and least known, Italian banking families still operative today.

Paolo Sarpi (1552-1623) was an Italian historian, prelate, scientist, canon lawyer, and statesman active on behalf of the Venetian Republic during the period of its successful defiance of the papal interdict and its war with Austria. He was one of the first and best propagandist. He published several pamphlets in defense of Venice’s rights over the Adriatic and the spread of the Venetian central banking system as a superior form of economics, government, and rulership.

Hans and Paul Berenberg founded the Berenberg Bank in Hamburg in 1590. Both brothers were Dutch refugees who joined the Hanseatic League. Berenberg Bank is the world’s oldest surviving merchant bank. The Berenberg banking family became extinct in the male line with Elisabeth Berenberg (1749-1822); she was married to Johann Hinrich Gossler, who became a co-owner of the bank in 1769. From the late 18th century, the Gossler family, as owners of Berenberg Bank, rose to great prominence in Hamburg, and was widely considered one of Hamburg’s two most prominent families.

Issachar Berend Lehmann (1661-1730) – was a German banker, merchant, diplomatic agent as well as army and mint contractor working as a court Jew for Elector Augustus II the Strong of Saxony, King of Poland, and other German princes. He was privileged as a Court Jew and as a Resident. Thanks to his wealth, privileges as well as social and cultural commitment he was a Jewish dignitary famous in his day in Central and Eastern Europe.

John Barker, Esq (1707-1787) was the Governor of the Crown-chartered monopoly London Assurance Company, secretly provided the capital to provision both the Continental and French Armies, then the capital to create Bank of North America (1781), Bank of New York (1784) and First Bank of the United States (1791) – all with Alexander Hamilton’s cooperation.

Barclays is a British multinational universal bank (1736), headquartered in London, England. Barclays operates as two divisions, Barclays UK and Barclays International, supported by a service company, Barclays Execution Services. Barclays traces its origins to the goldsmith banking business established in the City of London in 1690. James Barclay became a partner in the business in 1736. David and Alexander Barclay were engaged in the slave trade in 1756. In 1896, several banks in London and the English provinces, including Goslings Bank, Backhouse’s Bank and Gurney’s Bank, united as a joint-stock bank under the name Barclays and Co. Over the following years, Barclays expanded to become an international bank. Barclays has made numerous corporate acquisitions including Lehman Brothers in 2008.

Francis Baring (1740–1810) was a director of the British East India Company and founded Barings Bank in 1783. His sister Elizabeth married John Dunning who was a good friend of Lord Shelburne. Francis’ son Alexander, who married Ann Bingham, the granddaughter of Thomas Willing, formed Sun Alliance Assurance with Nathan Mayer Rothschild in 1824. The Barings were involved in running opium and slaves. Barings owned a slave plantation, and directed The British East India Company through Francis Baring, and The Bank of England through Alexander Baring. Alexander negotiated and financed The Louisiana Purchase. Barings financed the annexation of Texas from Mexico, and the purchase of Alaska from Russia. Barings financed Lincoln’s Ironclads ships and arms – essentially, arms dealers. Ultimately, HSBC was founded in 1866.

Mayer Amschel Rothschild (1744-1812) was a German banker and the founder of the Rothschild banking dynasty, which is believed to have become the wealthiest family in human history. He is often referred to as the “founding father” of the Rothschild banking dynasty.

John Barker Church (1748-1818) was also known as John Carter, a British Crown Agent handling and bankrolling Alexander Hamilton’s control of first U.S. banks: Bank of North America, First Bank of the United States, and Manhattan Company. He also bankrolled the commissary of the Continental and French Armies; his uncle was John Barker, Governor of the Crown-chartered London Assurance Company, the shipping insurance monopolist worldwide.

and slave owner of French origin. He personally saved the U.S. government from financial collapse during the War of 1812 and became one of the wealthiest people in America, estimated to have been the fourth richest American of all time. After the charter for the First Bank of the United States expired in 1811, Girard purchased most of its stock and its facilities on South Third Street in Philadelphia and reestablished it under his direct personal ownership. Philadelphia banks balked at accepting the notes that Girard issued on his personal credit and lobbied the state to force him to incorporate without success. Girard’s Bank was the principal source of government credit during the War of 1812. Girard placed nearly all of his resources at the disposal of the government and underwrote up to 95 percent of the war loan. After the war, he became a large stockholder in and one of the directors of the Second Bank of the United States. Girard’s bank ceased operations upon his death. Philadelphia businessmen, eager to cash in on Girard’s reputation opened a bank called the Girard Trust Company, and later Girard Bank. It merged with Mellon Bank in 1983 and was largely sold to Citizens Bank two decades later.

Alexander Hamilton (1755-1804) orchestrated British control of American banking from the inception of the republic. With Rothschild financing, Hamilton founded two New York banks including Bank of New York. He died in a gun battle with Aaron Burr, who founded Bank of Manhattan with Kuhn Loeb financing. Hamilton was the first in a series of banksters to hold the key position of Treasury Secretary.

In recent times Kennedy Treasury Secretary Douglas Dillon came from Dillon Read (UBS Warburg). Nixon Treasury Secretaries David Kennedy and William Simon came from Continental Illinois Bank (Bank of America) and Salomon Brothers (Citigroup). Carter Treasury Secretary Michael Blumenthal came from Goldman Sachs, Reagan Treasury Secretary Donald Regan came from Merrill Lynch (Bank of America), Bush Sr. Treasury Secretary Nicholas Brady came from Dillon Read (UBS Warburg) and both Clinton Treasury Secretary Robert Rubin and Bush Jr. Treasury Secretary Henry Paulson came from Goldman Sachs.

Aaron Burr, Jr. (1756-1836) was a British intelligence agent who became the U.S. Vice President (1801-1805) under Thomas Jefferson and co-founded the Manhattan Company with Alexander Hamilton and John Barker Church. Burr shot and killed (murdered) Hamilton in a duel on July 11, 1804.

Amschel Mayer Rothschild (1773-1855) was a German Jewish banker of the Rothschild family banking dynasty. He was the second child and eldest son of Mayer Amschel Rothschild, the founder of the dynasty.

Salomon Mayer von Rothschild (1774-1855) was a German-born banker who founded the Austrian branch of the prominent Rothschild family in Vienna, in 1820 by establishing the bank, S. M. von Rothschild.

Nathan Mayer Rothschild (1777-1836) was an German-English banker, businessman and financier. Born in Frankfurt am Main in Germany, he was the third of the five sons of Mayer Amschel Rothschild, and was of the second generation of the Rothschild banking dynasty. In 1798, Nathan was sent to England to further the family interests in textile importing with £20,000 capital (equivalent of £2.2 million). Nathan became a naturalized citizen in 1804 and established a bank in the City of London – N. M. Rothschild & Sons.

Carl Mayer von Rothschild (1788-1855) was a German-born banker in the Kingdom of the Two Sicilies and the founder of the Rothschild banking family of Naples.

Bank of North America (1781) is today known as Wells Fargo. Robert Morris was appointed by Congress to be the first superintendent of finance in 1781. Alexander Hamilton vied to be superintendent and was over-looked. Morris was successful in arranging for his British brother-in-law, John Barker Church, to become one of the Bank of North America’s two largest shareholders. While Church sailed to Europe to “settle wartime accounts” [and visit his London base of operations], Church named Hamilton his American business agent in his absence and “deputized” him to watch over his Bank of North America interests and establish the Bank of New York.

Sir Moses Haim Montefiore, 1st Baronet, (1784-1885) was a British financier and banker, activist, philanthropist and Sheriff of London who was born to an Italian Sephardic Jewish family based in London. He was the President of the Board of Deputies of British Jews. In 1812, Moses Montefiore married Judith Cohen, daughter of Levy Barent Cohen. Her sister, Henriette, married Nathan Mayer Rothschild, for whom Montefiore’s firm acted as stockbrokers. Nathan Rothschild headed the family’s banking business in Britain, and the two brothers-in-law became business partners. In business, Montefiore was an innovator, investing in the supply of piped gas for street lighting to European cities via the Imperial Continental Gas Association. In 1824 he was among the founding consortium of the Alliance Life Assurance Company, later Sun Alliance.

Johann Heinrich Schroder (1784-1883) founded Henry Schroder & Co. in London in 1818. J Henry Schroder Banking Corporation (‘Schrobanco’) was a commercial bank in New York founded in 1923. Schroder remained a British agent evidenced by Schroder issuing £3m bonds in 1863 for the Confederacy. Eventually, Schroders plc became a British multinational asset management company which was founded in 1804. The company now employs over 5,000 people worldwide in 32 locations around Europe, America, Asia, Africa and the Middle East. Headquartered in the City of London, it is traded on the London Stock Exchange and is a constituent of the FTSE 100 Index. The Schroder family, through trustee companies, individual ownership, and charities control 47 per cent of the company’s ordinary shares.

Bank of New York (1791) is today known as BNY Mellon. It was founded and directed by Alexander Hamilton and started with a deputization of Hamilton by his brother-in-law John Barker Church to start the bank with Church’s capital while he traveled to France and Britain to consolidate his fortune made from being the commissar for the Continental and French armies. Hamilton’s control of the Bank of North America, Bank of New York, and the U.S. Treasury gave him the power to decide that customs revenues could be paid not just in gold and silver but with notes from the Bank of New York and the Bank of North America.

First Bank of the United States (1791) is today known as BNY Mellon, Citizens. It was founded by Alexander Hamilton and its early stockholders included John Barker Church. By 1810, the British Alexander Baring and Rothschild & Sons Ltd. banks had acquired major stakes in the First Bank of the United States, as well as in the Bank of England. Another of the first stockholders includes Thomas M. Willing, who became the richest man in America. Willing served as president of the Bank of North America.

James “Jacob” Mayer de Rothschild (1792–1868) founded the Famille banquière Rothschild as a French banking dynasty in 1812, in Paris. James was sent to Paris from his home in Frankfurt, Germany, by his father, Mayer Amschel Rothschild. Mayer Amschel Rothschild had his eldest son remain in Frankfurt, while his four other sons were sent to different European cities to establish a financial institution to invest in business and provide banking services. Endogamy within the family was an essential part of the Rothschild strategy in order to ensure control of their wealth remained in family hands.

George Peabody (1795-1869) was an American financier and philanthropist. Peabody went into business in dry goods and later into banking. In 1837 he moved to London where he became the most noted American banker and helped to establish the young country’s international credit. Having no son of his own to whom he could pass on his business, Peabody took on Junius Spencer Morgan as a partner in 1854 and their joint business would go on to become J.P. Morgan & Co. after Peabody’s 1864 retirement. In 1837, Peabody took up residence in London, and the following year, he started a banking business trading on his own account. The banking firm of “George Peabody and Company” was established in 1851. It was founded to meet the increasing demand for securities issued by the American railroads, and – although Peabody continued to deal in dry goods and other commodities – he increasingly focused his attentions on merchant banking, specializing in financing governments and large companies. The bank rose to become the premier American house in London. Peabody, Morgan & Co. then took the name J.S. Morgan & Co. The former UK merchant bank Morgan Grenfell (now part of Deutsche Bank), international universal bank JPMorgan Chase and investment bank Morgan Stanley can all trace their roots to Peabody’s bank.

Upon Peabody’s retirement in 1864, control was assumed by Morgan who had joined the firm as a partner in 1854. The firm was renamed J. S. Morgan & Co. The firm’s New York agency was later to become J.P. Morgan & Co. under the leadership of Junius’ son J. Pierpont Morgan. On the death of Junius in 1890, Pierpont became the senior partner of the London firm. By 1910, all the firm’s Morgan family partners were resident in the U.S. and to reflect this the London partnership was restructured with J. P. Morgan & Co. in the U.S. assuming a 50% ownership of the London business which was reconstituted as Morgan Grenfell & Co. in recognition of the senior London-based partner, Edward Grenfell. JPMorgan Chase & Co. is now an American multinational investment bank and financial services holding company headquartered in New York City. As 2021, JPMorgan Chase is the largest bank in the United States, the world’s largest bank by market capitalization, and the fifth-largest bank in the world in terms of total assets, with total assets totaling to US$3.831 trillion.

The Warburg family founded MM Warburg & Co. in 1798, which makes it one of the oldest investment banks in existence. It was founded in 1798 by Banca Levi Kahana of Warburg and brothers Moses Marcus Warburg and Gerson Warburg. The Warburg family still owns the bank, continuing more than 200-years of private bank ownership. Siegmund George Warburg, James’ cousin, found the investment bank SG Warburg & Co of London in 1946, which later became UBS Warburg. Paul Warburg was a director of Wells Fargo. Wells Fargo is currently one of the four largest banks in the United States along with Bank of America, Citigroup and JP Morgan Chase. Paul Warburg, father of James Warburg, was one of the founders of the US Federal Reserve System, which still controls the American economy to this day. James Warburg’s uncle, Max Warburg, was among the main financiers of Lenin and the Bolshevik revolution, along with another powerful banker, Jacob Shiff.

The Manhattan Company (1799) is today known as J.P. Morgan Chase. It was promoted by Alexander Hamilton and Aaron Burr and was invested in by John Barker Church who became a director at Hamilton’s behest. The founders of the Manhattan Bank, Aaron Burr and John Barker Church, fought a duel on the very day of the founding of the bank. No one was hit, so they reconciled.

Brown Brothers & Co. (1818) is known today as Brown Brothers Harriman & Co. and is one of oldest and largest private investment banks in the United States. In 1931, the merger of Brown Brothers & Co. (founded in 1818) and Harriman Brothers & Co. formed the current BBH. After immigrating to Baltimore in 1800 and building a successful linen mercantile trading business, Alexander Brown and his four sons co-founded Alex. Brown & Sons. In 1818, one son, John Alexander Brown, traveled to Philadelphia to establish John A. Brown and Co. In 1825, another son, James Brown, established Brown Brothers & Co. on Pine Street in Lower Manhattan and relocated to Wall Street in 1833.

This firm eventually acquired all other Brown branches in the U.S. Another son, William Brown, had established William Brown & Co. in England in 1810, which was renamed Brown, Shipley & Co. in 1839 and became a separate entity in 1918.

On January 2, 1931, Brown Brothers & Co. merged with two other business entities, Harriman Brothers & Company, a private bank started with railway money, and W. A. Harriman & Co. to form Brown Brothers Harriman & Co. Founding partners included: Prescott Bush, E. Roland Harriman, and W. Averell Harriman. In 1930s the company acted as a U.S. base for the German industrialist Fritz Thyssen, who helped finance Adolf Hitler. Later, Prescott Bush would become one of the seven directors of the Union Banking Corporation in the US whose assets were seized by the United States government on October 20, 1942, during World War II under the U.S. Trading with the Enemy Act.

Marcus Goldman (1821-1904) was an American investment banker, businessman, and financier. He was born into an Ashkenazi Jewish family in Trappstadt, Germany, and immigrated to the United States in 1848. His paternal grandfather was called Jonathan Marx until he changed his name to Goldmann when Jews were allowed to have surnames in 1811. While attending classes at the synagogue in Wurzburg, he met Joseph Sachs, who would become his lifelong friend. Goldman immigrated to the United States from Frankfurt am Main, Germany, in 1848. Upon his arrival in America, his name was changed to Marcus Goldman by US immigration. He was the founder of Goldman Sachs, which has since become one of the world’s largest investment banks. Marcus Goldman founded Goldman Sachs in New York City, in 1869. In 1882, Goldman’s son-in-law Samuel Sachs joined the firm. In 1885, Goldman took his son Henry and his son-in-law Ludwig Dreyfuss into the business and the firm adopted its present name, Goldman Sachs & Co. The company has been criticized for a lack of ethical standards, working with dictatorial regimes, cozy relationships with the US federal government via a “revolving door” of former employees, and driving up prices of commodities through futures speculation, to mention a few of the hundreds of cases of corruption.

Solomon Loeb (1828-1903) was a German-born American banker and businessman. He was a merchant in textiles and later a banker with Kuhn, Loeb & Co.

John Pierpont Morgan (1837-1913) was an American financier and investment banker who dominated corporate finance on Wall Street throughout the Gilded Age. As the head of the banking firm that ultimately became known as J.P. Morgan and Co., he was the driving force behind the wave of industrial consolidation in the United States. Over the course of his career on Wall Street, J.P. Morgan spearheaded the formation of several prominent multinational corporations including U.S. Steel, International Harvester, and General Electric. He and his partners also held controlling interests in numerous other American businesses including Aetna, Western Union, Pullman Car Company, and 21 railroads. His son, J. P. Morgan Jr., took over the business at his father’s death, but was never as influential.

As required by the 1933 Glass–Steagall Act, the “House of Morgan” became three entities: J.P. Morgan & Co., which later became Morgan Guaranty Trust; Morgan Stanley, an investment house formed by his grandson Henry Sturgis Morgan; and Morgan Grenfell in London, an overseas securities house.

John Davison Rockefeller Sr. (1839-1937) was an American business magnate and philanthropist. He is widely considered the wealthiest American of all time and the richest person in modern history. Rockefeller founded the Standard Oil Company in 1870. He ran it until 1897 and remained its largest shareholder. Rockefeller’s wealth soared as kerosene and gasoline grew in importance, and he quickly became the richest person in the country, controlling 90% of all oil in the United States at his peak. This was typical of Robber Barons who were given monopolies via the federal government.

Jacob Henry Schiff (1847-1920) was an American banker, businessman, and philanthropist who helped finance, among many other things, the Japanese military efforts against Tsarist Russia in the Russo-Japanese War.

James Loeb (1867-1933) was a German-born American banker, Hellenist, and philanthropist.

Paul Moritz Warburg (1868-1932) was a German-born American banker who was an early advocate of the U.S. Federal Reserve System.

Amadeo P. Giannini (1870-1949) founded the Bank of Italy in San Francisco, California, in 1904. It grew by a “branch banking” strategy to become Bank of America, the world’s largest commercial bank. The Bank of Italy merged with a smaller Bank of America in Los Angeles during 1928. In 1930, Giannini changed the name “Bank of Italy” to “Bank of America.” As chairman of the new, larger Bank of America, Giannini expanded the bank throughout his tenure, which continued until his death in 1949. Bank of America merged with NationsBank of Charlotte, North Carolina, in 1998.

Felix Moritz Warburg (1871-1937) was a German-born American banker. He was a member of the Warburg banking family of Hamburg, Germany.

Mortimer Loeb Schiff (1877-1931) was an American banker and notable early Boy Scouts of America leader. His son John Mortimer Schiff was also involved with the BSA.

James Paul Warburg (1896-1969) was a German-born American banker who was well known for being the financial adviser to Franklin D. Roosevelt. His father was banker Paul Warburg, member of the Warburg family who helped found the US Federal Reserve.

Sir Siegmund George Warburg (1902-1982) was a German-born English banker. He was a member of the prominent Warburg family. He played a prominent role in the development of merchant banking both in England and America.

David Rockefeller (1915-2017) was an American investment banker who served as chairman and chief executive of Chase Manhattan Corporation. He was the oldest living member of the third generation of the Rockefeller family and family patriarch from July 2004 until his death in March 2017. David was the fifth son and youngest child of John D. Rockefeller Jr. and Abby Aldrich Rockefeller, and a grandson of John D. Rockefeller. He was noted for his wide-ranging political connections and foreign travel, in which he met with many foreign leaders. His fortune was estimated at $3.3 billion at the time of his death in March 2017.

US Federal Reserve System is the central banking system of the United States of America enacted by the Federal Reserve Act of 1913. The U.S. Congress established three key objectives for monetary policy in the Federal Reserve Act: maximizing employment, stabilizing prices, and moderating long-term interest rates. Its duties have expanded over the years, and currently also include supervising and regulating banks, maintaining the stability of the financial system, and providing financial services to depository institutions, the U.S. government, and foreign official institutions.

The Federal Reserve System is governed by the presidentially-appointed board of governors, or Federal Reserve Board. Twelve regional Federal Reserve Banks, located in cities throughout the nation, regulate and oversee privately owned commercial banks. Nationally chartered commercial banks are required to hold stock in, and can elect some board members of, the Federal Reserve Bank of their region. The Federal Open Market Committee sets monetary policy through its seven members of the board of governors and the twelve regional Federal Reserve Bank presidents. United States Department of the Treasury, an entity outside of the central bank, prints the currency used.

Although an instrument of the US Government, the Federal Reserve System considers itself “an independent central bank because its monetary policy decisions do not have to be approved by the President or by anyone else in the executive or legislative branches of government, it does not receive funding appropriated by Congress, and the terms of the members of the board of governors span multiple presidential and congressional terms.”

The Bank for International Settlements was founded in 1930 and is owned by the US Federal Reserve, Bank of England, Bank of Italy, Bank of Canada, Swiss National Bank, Nederlandsche Bank, Bundesbank, and Bank of France. The BIS is the most powerful bank in the world and is a global central bank for the Banking Families who control the private central banks of almost all Western and developing nations. The first president of BIS was Rockefeller banker Gates McGarrah – an official at Chase Manhattan and the Federal Reserve. The US government had a historical distrust of BIS, lobbying unsuccessfully for its demise at the 1944 post-WWII Bretton Woods Conference. Instead, the Banking Families’ power was compounded with the Bretton Woods creation of the IMF and the World Bank.

The BIS holds at least 10% of monetary reserves for at least 80 of the world’s central banks, the IMF, and other multilateral institutions. It serves as financial agent for international agreements, collects information on the global economy and serves as lender of last resort to prevent global financial collapse. The BIS promotes an agenda of monopoly capitalist-fascism. It serves as the conduit for the Banking Families who funded Adolf Hitler. This effort was led by the Warburg’s J. Henry Schroeder and Mendelsohn Bank of Amsterdam. In 1944, the first World Bank bonds were floated by Morgan Stanley and First Boston which helped support the World Trade Organization, International Monetary Fund, and the World Economic Forum.

The World Bank is an international financial institution that provides loans and grants to the governments of low- and middle-income countries for the purpose of pursuing capital projects. The World Bank is the collective name for the International Bank for Reconstruction and Development and the International Development Association, two of five international organizations owned by the World Bank Group. It was established along with the International Monetary Fund at the 1944 Bretton Woods Conference along with the International Monetary Fund. The president of the World Bank is traditionally an American. The World Bank and the International Monetary Fund are both based in Washington, D.C., and work closely with each other. Although many countries were represented at the Bretton Woods Conference, the United States and United Kingdom were the most powerful in attendance and dominated the negotiations.

REPUBLIC OF VENICE – CENTRAL BANK MODEL

The central banking system of Venice had a committee of Ten who oversaw the “Republic” while an inner subset of that committee was the committee of Three, who had the power to order the death of anyone who might be harming the Republic, the City-state of Venice. The power of death was given to bankers as well as the power to imprison people who did not repay loans on time – debtors prison. Bankers became powerful forces in the lives of those who used them; and as time wore on, bankers entered into every aspect of personal and civic life. Bankers came to control not only land and money, but also became civil and political powerhouses who controlled life and death circumstances. Eventually, banking became synonymous with corruption, evil, subterfuge, propaganda, espionage, war, demonic practices, and punitive laws.

Looking objectively at the history of money and banking is an exploration of the worship of anti-human forces that have created some of the worst pages in history. That is why we use the derogatory term “banksters” as an indication that these bankers are economic gangsters who will not hesitate to kill through war, starvation, and economic slavery. The Venetians forgot what King Hammurabi learned when he made laws concerning the periodic forgiveness of loans because generally, the common person could not pay back the debt and the interest on the loan, therefore necessitating time in debtors prison when the loans default. When usury filled up Hammurabi’s jails, he learned to grant a loan forgiveness celebration every three years. The Hebrews called it the “Year of Jubilee” and forgave all loans made to other Hebrews every seven years. The lesson learned is the same as 4,000 years ago; usuary doesn’t work.

BRITISH BANKSTERS

The oligarchical banking system of Great Britain represents a refined model of the traditions of the Babylonians, Romans, Byzantines, and Venetians which have been transplanted into the British Isles through a series of upheavals. In the sixteenth and seventeenth century the evil of Venetian Mammon worship invaded England and Scotland through the Venetian oligarchy and its philosophy, political forms, family fortunes, and imperial geopolitics. The victory of the Venetian party in England between 1509 and 1715 built upon the Byzantine and Venetian banking foundation.

Venetian oligarchs were a guiding force among the Lombard bankers who carried out the “great shearing” of England which led to the bankruptcy of the English King Henry III, who, during the 1250’s, repudiated his debts and went bankrupt. The bankruptcy was followed by a large-scale civil war. It was under Venetian auspices that England started the catastrophic conflict against France known today as the Hundred Years War. In 1340, King Edward III of England sent an embassy to Doge Gradenigo announcing his intention to wage war on France and proposing an Anglo-Venetian alliance. Gradenigo accepted Edward III’s offer that all Venetians on English soil would receive all the same privileges and immunities enjoyed by Englishmen. The Venetians accepted the privileges and declined to join in the fighting. Henry VII’s suppression of the oligarchs displeased Venice.

The Venetians wanted England to become embroiled with both France and Spain. Venice was also fundamentally hostile to the modern nation-state, which Henry was promoting in England. When Henry VII’s son Henry VIII turned out to be a pro-Venetian and the Venetians were able to re-assert their oligarchical system.

Henry VIII was King of England between 1509 and 1547. His accession to the throne coincided with the outbreak of the War of the League of Cambrai, in which most European states, including France, the Holy Roman Empire (Germany), Spain, and the papacy of Pope Julius II joined together in a combination that tried to annihilate Venice and its oligarchy. Henry VIII alone among the major rulers of Europe, maintained a pro-Venetian position. Henry VIII was for a time the formal ally of Venice and Pope Julius.

In 1527, when Henry VIII sought to divorce Catherine of Aragon, the Venetian-controlled University of Padua endorsed Henry’s legal arguments. Gasparo Contarini, the dominant political figure of the Venetian oligarchy, sent to the English court a delegation which included his own uncle, Francesco Zorzi. The oligarch and intelligence operative Zorzi, consummately skilled in playing on Henry’s lust and paranoia, became the founder of the powerful Freemasonic tradition in the Tudor court. Later, Henry VIII took the momentous step of breaking with the Roman Papacy to become the “New Constantine” and founder of the Anglican Church. He did this under the explicit advice of Thomas Cromwell, a Venetian agent who had become his chief adviser. Thomas Cromwell was Henry VIII’s business agent in the confiscation of the former Catholic monasteries and other church property, which were sold off to rising families. Thomas Cromwell thus served as the midwife to many a line of oligarchs.

The Venetian oligarchy (especially its “giovani” faction around Paolo Sarpi) responded by transferring its family fortunes, philosophical outlook, and political methods into England as the most suitable site for the New Venice, the future center of a new, world-wide Roman Empire based on maritime supremacy.

The Venetians insisted on the maintenance of a Protestant dynasty and a Protestant state church in England, with an anti-Spanish policy. Many of these successful measures were coherent with the Venetian desire to build up England as the new world empire and as a counterweight to the immense power of Spain. For the Venetians, an oligarchy required the weak executive power of a Doge [prince or monarch], and this was the system they wanted transplanted into their clone, England. England was the country where the triumph of the oligarchs was eventually most complete. Parliamentary leaders wanted to establish an oligarchy by the surrender of the King to Parliament so they could build up a navy and hasten the looting of the Spanish Empire.

Oliver Cromwell was a Venetian agent. Prominent in Oliver Cromwell’s family tree was the widely hated Venetian agent Thomas Cromwell. Oliver Cromwell (1599-1658) was descended from Thomas Cromwell’s sister. Oliver Cromwell’s uncle had married the widow of the Genoese-Venetian financier Sir Horatio Pallavicini. This widow brought two children by her marriage to Pallavicini and married them to her own later Cromwell children. So, the Cromwell family was intimately connected to the world of Venetian finance.

In March 1655, Cromwell decided in favor of a “thorough” Bonapartist military dictatorship similar to a sovereign republic of Italy with the Doge. The Anglo-Venetians decided that they were fed up with the Catholic, pro-French Stuart dynasty. Representatives of some of the leading oligarchical families signed an invitation to the Dutch King, William of Orange, and his Queen Mary, a daughter of James II. This is called by the British, the “Glorious Revolution” of 1688; in reality, it consolidated the powers and prerogatives of the oligarchy, which were expressed in the Bill of Rights of 1689. No taxes could be levied, no army raised, and no laws suspended without the consent of the oligarchy in Parliament. Parliament was supreme over the monarch and the state church. Within a few years after the Glorious Revolution there was a Bank of England and a national debt. When George I ascended the throne in 1714, he knew he was a Doge, the leader of an oligarchy.

The regime that took shape in England after 1688 was the most perfect copy of the Venetian oligarchy that was ever produced. The Venetian Party was broadly hegemonic, and Britain was soon the dominant world power. The struggles of seventeenth-century England were thus decisive in parlaying the strong Venetian influence which had existed before 1603 into the long-term domination by the British Venetian Party, observable after 1714. These developments are not phenomena of English history per se. They can only be understood as aspects of the infiltration into England of the metastatic Venetian oligarchy, which in its British Imperial guise has remained the menace of mankind.

THE WARBURG BANKSTERS

The Warburg family had settled in Venice, at which point they bore the surname del-Banco. The historical documents describe Anselmo del Banco as Jewish and as having been one of the wealthiest residents of Venice in the early 16th century. In 1513, del Banco was granted a charter by the Venetian government permitting the lending of money with interest. Del Banco left with his family after new restrictions were placed upon the Jewish community coinciding with the establishment of a Jewish ghetto. The family settled in Bologna, and from there to the German town of Warburg and adopted that town’s name as their own surname.

The Warburg family re-established itself in Altona, near Hamburg in the 17th century, and it was there that M. M. Warburg & Co. was established in 1798, among the oldest still existing investment banks in the world. Other banks created by members of the family include: M.M.Warburg & Co., Warburg Pincus, S. G. Warburg & Co., and UBS Warburg.

The family is traditionally divided into two prominent lines, the Alsterufer Warburgs and the Mittelweg Warburgs. The Alsterufer Warburgs descended from Siegmund Warburg (1835-1889) and the Mittelweg Warburgs descended from his brother Moritz M. Warburg (1838-1910). They took their nicknames from the brothers’ respective addresses in Hamburg’s Rotherbaum neighborhood. The brothers were grandsons of Moses Marcus Warburg. Siegmund George Warburg was of the Alsterufer line; the five brothers Abraham M., Max M., Paul M., Felix M. and Fritz Moritz Warburg were of the Mittelweg line.

The brothers Moses Marcus Warburg (1763-1830) and Gerson Warburg (1765-1826) founded the M. M. Warburg & Co. banking company in 1798. Moses Warburg’s great-great grandson, Siegmund George Warburg, founded the investment bank S. G. Warburg & Co in London in 1946. Siegmund’s second cousin, Eric Warburg, founded Warburg Pincus in New York in 1938. Eric Warburg’s son Max Warburg is currently one of the three partners of M. M. Warburg & Co. Max Warburg’s elder brother Aby Warburg used his money to establish the Kulturwissenschaftliche Bibliothek Warburg in Hamburg, since 1934, and the Warburg Institute in London. Paul Warburg is most famous as an advocate of the US Federal Reserve System, established in 1913.

Felix and Paul Warburg emigrated to the United States. Felix Warburg married Frieda Schiff, daughter of Jacob H. Schiff, a banker who grew up in Frankfurt. Schiff financed parts of the American rail system through his investment bank Kuhn Loeb. Felix Warburg’s house in New York City is now the Jewish Museum, and Kfar Warburg in Israel is named for him. His brother Paul Warburg married Nina Loeb, daughter of Solomon Loeb. Paul Warburg was a major planner for the U.S. Federal Reserve System in 1913. He attended as the American representative, at the Treaty of Versailles conference, where his brother Max was on the German side of the bargaining table.